Bicycles are more than just a mode of transport in India; for millions, especially in rural and low-income households, they are a lifeline. They're the means to get to work, school, market, and access essential services. But what happens when this crucial asset breaks down or needs repairs? As the data from the Household Consumption Expenditure clearly shows, it can be a significant financial burden, especially for those who can least afford it.

Let's dive into the numbers and understand why microinsurance for bicycles isn't just a good idea, but a vital necessity.

Bicycles: A Widespread Lifeline, Especially for the Vulnerable

42% of Indian households possess bicycles, where the percentage for rural households stands at more than 50% and for urban households it is nearly 27% (see Table 1). Breaking down the numbers across income quintiles reveals compelling story about bicycle ownership across India:

- Higher Ownership Among Lower-Income Households:

The lowest income quintile (0-20%) shows the highest bicycle possession, 32.29% at all India level with 37.53% of rural households and 13.08% of urban households owning a bicycle. This starkly highlights that bicycles are disproportionately relied upon by those with fewer resources. - Rural Reliance:

Rural areas consistently show higher bicycle ownership across all income groups compared to urban areas, underscoring their critical role in rural mobility and livelihoods.

Table 1: Possession of Bicycle in different quintile MPCE classes separately for rural and urban areas in India Rural Urban All India 0–20% 37.53 13.08 32.29 20–40% 27.84 16.53 25.42 40–60% 18.54 19.46 18.74 60–80% 11.7 25.01 14.55 80–100% 4.38 25.92 9 Total 50.11 27.07 42.38 Source: Calculated using Household Consumption Expenditure Round 2023-24.

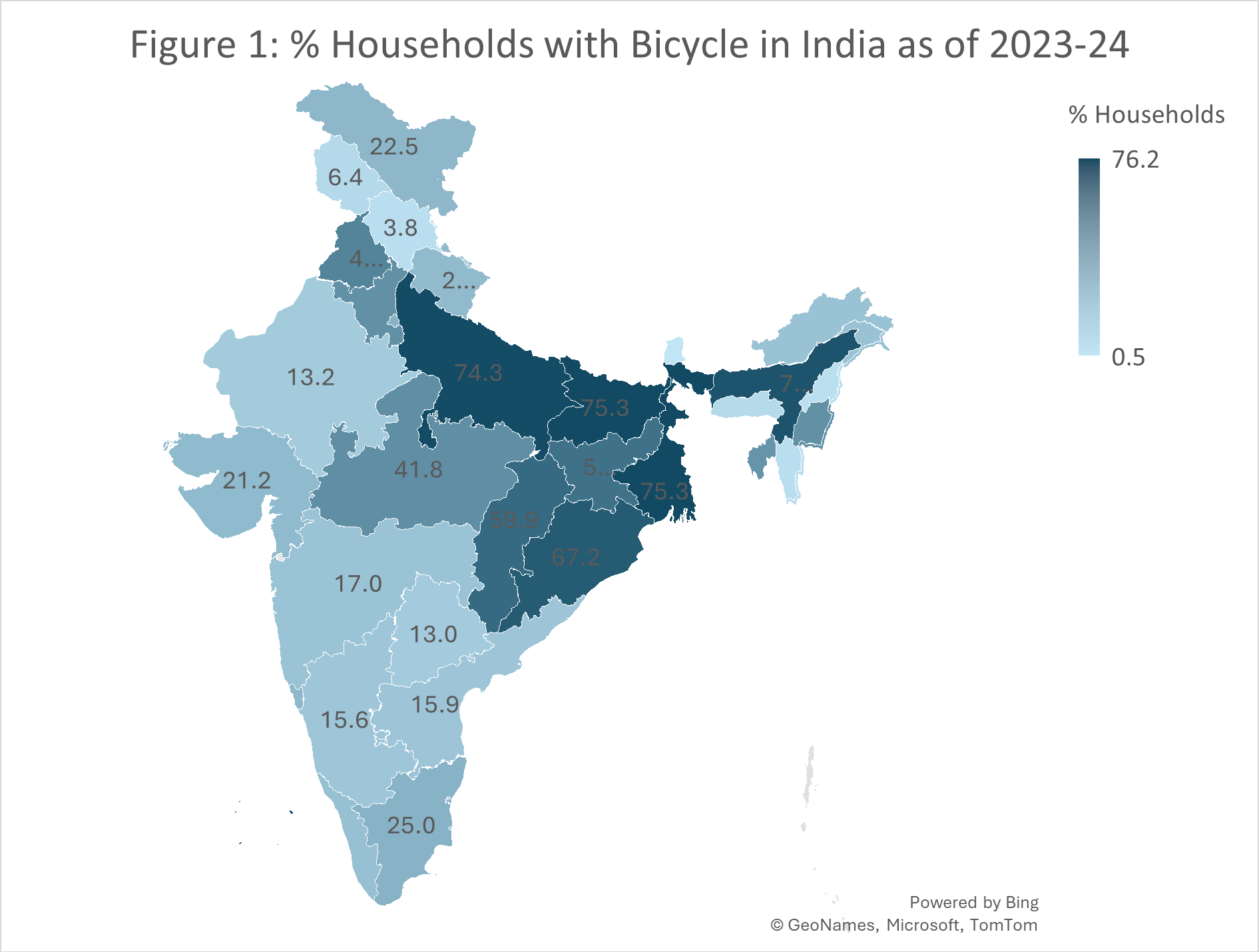

This data paints a clear picture: bicycles are an essential asset for a significant portion of India's low-income population. The distribution of bicycle varies significantly across Indian states. West Bengal and Bihar has the highest percentage of households owning bicycles at 75.3 percent, followed by Uttar Pradesh with 74.3 percent, Assam with 70.8 percentage and Odisha with 67.2 percent (see Figure 1).

The Hidden Costs: Repairs and Maintenance are a Real Burden

While the initial cost of a bicycle might be manageable, the ongoing expenses of repairs and maintenance often go overlooked. The data extracted leveraging Household Consumption Expenditure 2023-24 sheds light on this crucial aspect:

- Substantial Repair Costs:

The average cost of repair & maintenance across all quintiles and regions to repair and maintain bicycle are not negligible. For the lowest income group (0-20%), the average cost of repair is Rs. 359 in rural areas and Rs. 380 in urban areas (see table 2). While these numbers might seem small to some, for households living on tight budgets, this can be a significant setback.

Table 2: Average Cost (Rs.) of repair & maintenance of Bicycle in Rural and Urban by quintile class of UMPCE Rural Urban All India 0–20% 359 380 362 20–40% 360 378 364 40–60% 344 359 348 60–80% 357 352 355 80–100% 374 385 382 Source: Calculated using Household Consumption Expenditure Round 2023-24.

- Cost as Percentage of Bicycle Value:

The cost towards keeping their bicycle running, every household have to spend 10-17% of the value to bicycle in rural areas and 8-13% in urban areas (see Table 3) with a range of the cost going beyond 100 percentage for some households indicating the cost of keep running the bicycle exceeds the total value of the bicycle itself. This is a substantial chunk of their very limited disposable income. A broken bicycle can mean lost wages, missed school, or inability to access essential services like healthcare or ration shops.

| Table 3: Percentage Cost of repair & maintenance of Bicycle to Total Value of Bicycle in Rural and Urban by quintile class of UMPCE | |||

| Rural | Urban | All India | |

|---|---|---|---|

| 0–20% | 10 | 12 | 10 |

| 20–40% | 20 | 10 | 17 |

| 40–60% | 17 | 13 | 16 |

| 60–80% | 11 | 8 | 10 |

| 80–100% | 10 | 9 | 9 |

The Case for Microinsurance: A Shield Against Financial Shocks

Given these realities, the need for a safety net becomes glaringly obvious. This is where bicycle microinsurance comes in.

Microinsurance, designed specifically for low-income populations with affordable premiums and simple claim processes, can offer:

1.Financial Protection:

Imagine a scenario where a sudden puncture

or a broken chain means sacrificing a day's wages or cutting back on essential

food items. Microinsurance can cover these repair costs, preventing a minor

incident from snowballing into a major financial crisis.

2.Livelihood Security:

For many, the bicycle is directly linked to

their livelihood for a delivery rider, a daily wage labourer, or a farmer

transporting produce. Insurance ensures that a broken bicycle doesn't equate to

lost income and economic instability.

3.Peace of Mind:

Knowing that their vital mode of transport is

protected offers invaluable peace of mind to these vulnerable households. It

allows them to focus on earning and living, rather than constantly worrying

about unexpected repair expenses.

4.Promoting Sustainable Transport:

By making bicycle ownership more

resilient, microinsurance can indirectly encourage the continued use of this

eco-friendly and affordable mode of transport, contributing to sustainable

development goals.

Moving Forward: A Call to Action

The data clearly demonstrates that bicycles are indispensable for low-income households in India, and the costs associated with their upkeep are a real burden. There is a strong and undeniable case for the widespread adoption and promotion of bicycle microinsurance.

The data clearly demonstrates that bicycles are indispensable for low-income households in India, and the costs associated with their upkeep are a real burden. There is a strong and undeniable case for the widespread adoption and promotion of bicycle microinsurance.

It's time for insurance providers, NGOs, and government bodies to collaborate and develop innovative, accessible, and affordable microinsurance products tailored to the needs of these communities. By doing so, it can be ensured that the wheels of progress keep turning for everyone, especially those who rely on this humble yet powerful mode of transport to build a better life.

Conclusion:

In essence, bicycles are an indispensable lifeline for millions of low-to-middle income Indian households. With repair costs consuming significant chunk of expenditure, unexpected breakdowns pose a significant financial threat. Bicycle microinsurance offers a critical solution, providing essential financial protection, securing livelihoods, and offering much-needed peace of mind. It is imperative for stakeholders to collaborate on accessible, affordable microinsurance products, ensuring this vital mode of transport continues to empower communities and drive progress.

About MicroInsurance Innovation Hub Foundation

The MicroInsurance Innovation Hub (MIIH) Foundation aims to revolutionize the Microinsurance segment, especially in India and the Asia Pacific region. Based in Hyderabad, it focuses on developing inclusive insurance solutions tailored to underserved populations. By exploring product, technological, and process requirements, the hub supports interested companies in penetrating this market segment. With a mission to serve the underprivileged, it strives to enhance insurance penetration and foster inclusive growth.

The Hub would work to support the development of micro insurance in the Indian insurance industry through exploring various aspects of this business, the product range, the technological requirements, the process requirements, and the type of people required to enhance penetration. For more information write us at contact@microinsuranceinnovation.com

Disclaimer:

The Microinsurance Innovation Hub (MIIH) Foundation is a Section 8 company and has members who intend to foster financial inclusion of underserved and unserved communities through providing Insurance. The innovation hub will act as an open platform to the stakeholders of microinsurance. This Hub will exclusively work in the Microinsurance / Inclusive Insurance space in India and other regions. The information provided here is gathered from various sources and Microinsurance Innovation Hub doesn’t validate any data. The information here are intended solely for internal discussion purposes.